It was the best of times, it was the worst of times: After the COVID-19 pandemic, the British economy seemed to outpace Europe. With a swift economic recovery, steadily growing GDP, and low unemployment rates, the U.K. pulled ahead of many of its European and global competitors. Yet, the rapid GDP growth is nothing more than a Potemkin village — hiding excess debt and low productivity behind a façade.

But what exactly is so concerning about the current state of the British economy? How does it uphold the façade of a well-performing economy? And what happens once the façade falls? The issues started with the 2008 financial crisis, and a subsequent reluctance to invest in productivity and real-wage development.

It was the age of wisdom…

The United Kingdom is seemingly thriving. The global recession prompted by the COVID-19 pandemic meant a plunge in performance for almost all economies across the globe, but the British economy swiftly caught up afterward. After the 2020 recession, the economy bounced back in 2021 with a stunning 8.6% growth. In comparison, the biggest industrial European powers, France and Germany, grew slower than 2%. This trend persisted in 2022, with the British economy outpacing its European counterparts.

Even better, unemployment fell faster than in any other European country. While unemployment increased during the pandemic to 5.2%, it fell back to 4.2% again within two years. Similarly, the post-pandemic inflation has recovered from a peak of 11% back to 2.2%, and exports are at an all-time high of $1,032.61 billion.

All these figures paint a rather positive picture, one that other European countries ought to admire and imitate. Or should they?

… it was the age of foolishness

While the rapid recovery of the economy and low unemployment rates portray the U.K. as a well-off country, two indicators reveal the true state of the British economy: public debt and productivity.

One alarming indicator is the amount of public debt: Before the crisis, the public sector debt-to-GDP was 80%, and it had steadily been improving from the peak of 85% in 2017. However, during the pandemic, this level of debt rushed to 100%. Anti-epidemic measures alone are estimated to have cost around £350 billion (US$ 452.11 bn), but the most impactful policies were tax cuts to uphold consumption levels, and economic support programs that are estimated to have cost 3.2 billion pounds. So, while tax revenues saw a decline of 7.8%, spending increased, which resulted in the highest government deficit since World War II — contrary to predictions of declining debt made by economic experts and the IMF. As of now, the debt-to-GDP ratio still floats around 100%, with a growing tendency. What happened?

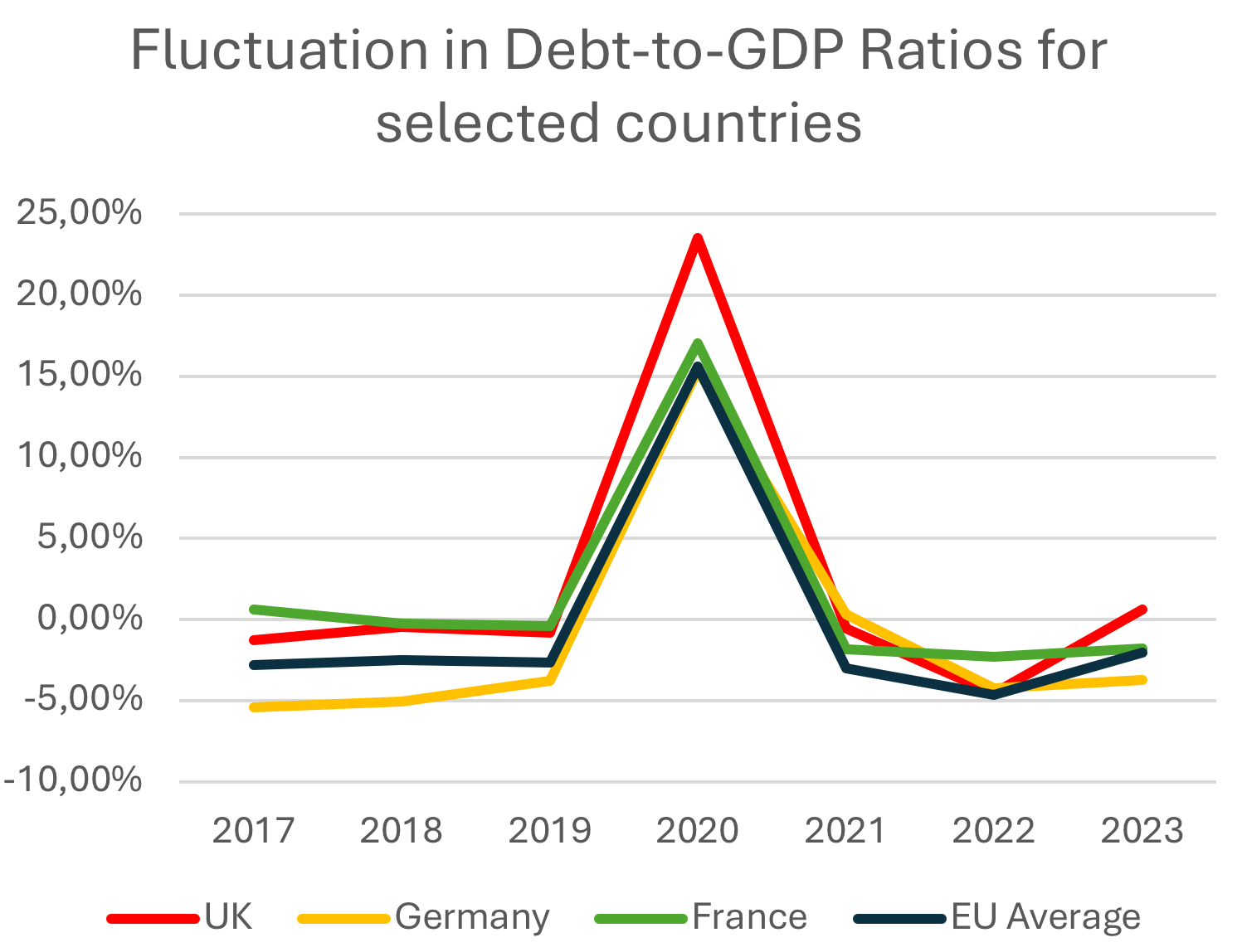

Chart: Henry Krenzer, Source: Eurostat

1: Debt to GDP Ratio fluctuation for the UK, Germany, France, and the EU Average

The natural British reaction to the pandemic, as in most other European economies, was excess government spending to keep the economy afloat. However, post-pandemic, the U.K. did not keep up with the fiscal discipline of its European neighbors. Most big economies significantly reduced their debt burden, often undergoing significant strain to do so. In the first year after the pandemic, we can see efforts of debt repayment in the U.K., but in 2022, debt-to-GDP began increasing again. Instead of saving money, the UK even slid further into debt.

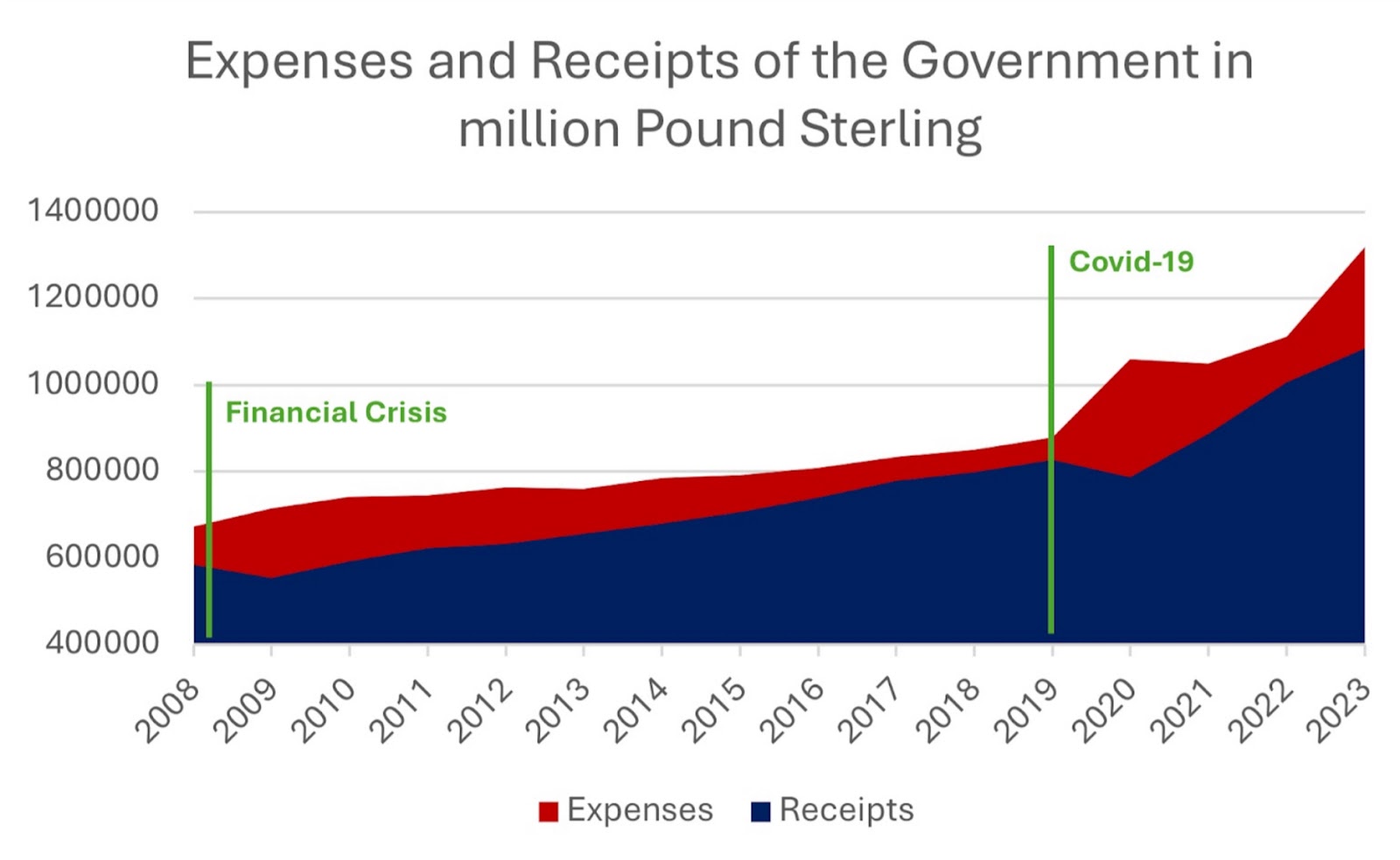

Chart: Henry Krenzer, Source: Office for National Statistics, Expenses and Receipts

2: Expenses and Receipts of the British Government in million £

The issue was not necessarily on the spending side: Government spending remained constant at around 42% of GDP annually through the past three years. What declined was the government income, mainly through taxation. Shortly after the end of the end of the crisis, the UK almost slid into recession and only scored a 0.6% GDP growth for 2023. This is for two main reasons: production inefficiency and historical debt burdens.

Productivity in terms of GDP per hour grew by 2% on average until 2008. After plummeting during the 2008 financial crisis, productivity stagnated for the next nine years and only surpassed the level of 2008 in 2017. And even since then, productivity has grown only by 0.8% annually. In global comparison, the U.K. is also lagging behind major European powers and the U.S. by almost 20%.

A key reason for this productivity lag is the inappropriate reaction of the British government to the financial crisis. The British economy opted for austerity and was careful not to increase public spending (except to bail out several banks). Trying to compensate for 137 billion pounds in additional expenses, the government refused to lower taxes. Additionally, it did not increase minimum wages, fearing this might hamper employment. In many ways, this austerity came at the wrong time and led to a series of unfavorable reactions on the labor market: real wage stagnation, a skill-mismatch, and lack of innovation, often referred to as the “productivity puzzle.”

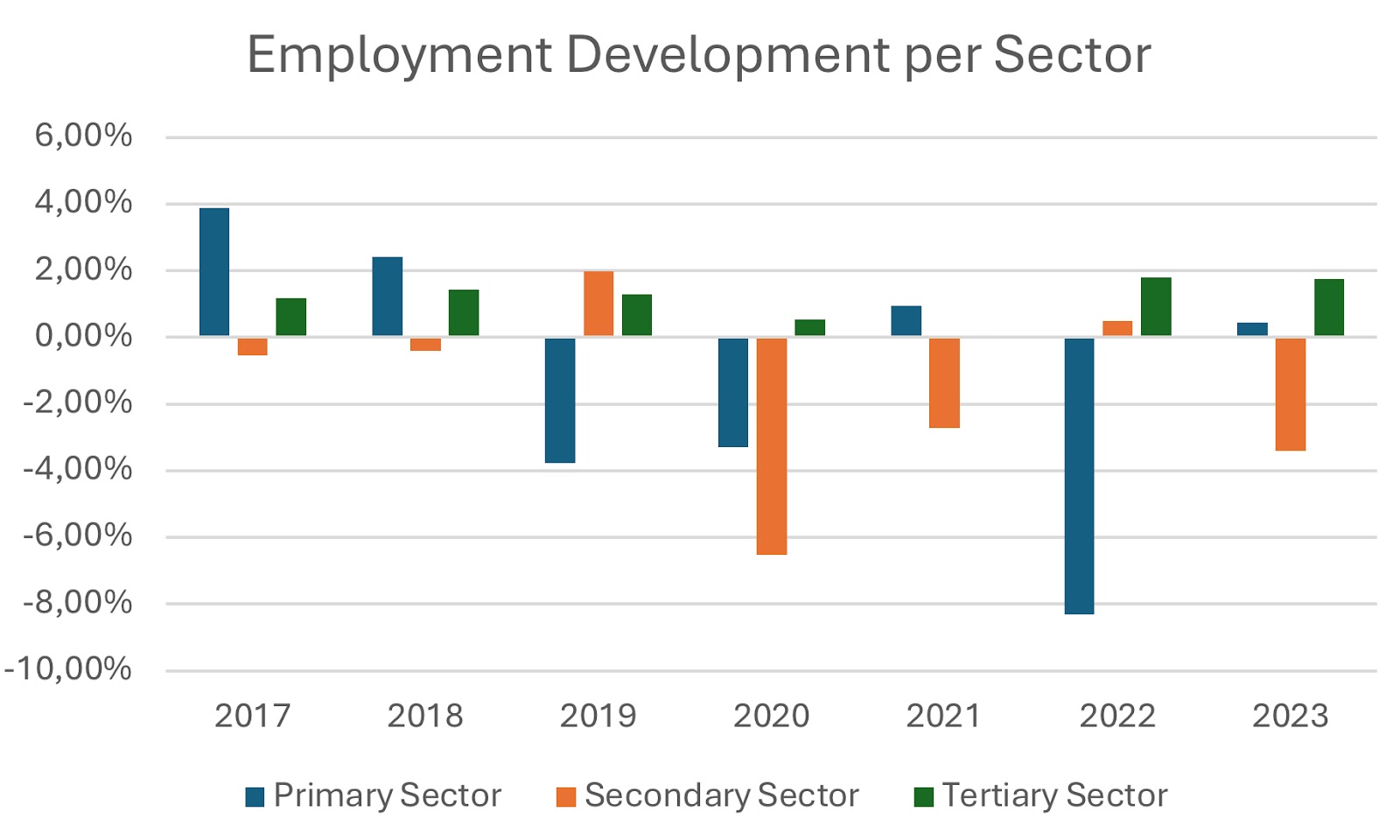

Chart: Henry Krenzer, Source: Office for National Statistics

3: Employment Changes between 2017-2023 per employment sector

The above graph shows the rate of re-employment in the three different sectors of the British economy after the pandemic. While the service-sector saw the biggest post-crisis increase, it is also the sector with the lowest marginal productivity. As many people looked for economic opportunities, they did not find them in their original sector, and had to take up work in a sector that did not match their qualifications, effectively doubling the skill mismatch. The crisis put households and companies under pressure, and the lack of government spending exacerbated this issue by neglecting necessary investments in labor productivity, education and wage standards.

What upheld the facade was the growing GDP, driven by high employment and financed through cheap loans. However, the unexpected increase of interest rates on the ill-allocated loans made these loans an expensive trap. Although financing investments in times of crisis through debt is helpful, investing in assets that will not increase long-term productivity and development is a losing game.

This is not a new story: In the 1990s, Japan fell into a similar limbo. Falling labor productivity prompted a decline in household disposable income, throwing the economy in a vicious cycle of falling consumption and investments. Although Japan was able to turn the economy around at the turn of the century by increasing bond-funded government expenditure, Japan still holds one of the highest debt ratios in the world. This is a fate that the British economy ought to avoid.

The economy of the United Kingdom will not fail overnight. But it is ailing from wounds that it suffered over ten years ago. Instead of addressing root causes directly, the U.K. has mistakenly been treating the symptoms. The array of crises in the past four years allowed for a renewed outbreak, which can only be contained by a combination of fiscal discipline, and focusing investments on areas that allow for sustainable innovation and, most importantly, real wage growth.

The British government should be wise and disciplined about where it spends its money. If not, it’s in for a rude awakening.